The most important thing was how to manage the chorus activities of finance under such situations like- Payment to Contractors and Suppliers including small vendors, as there was nothing ready for accepting the challenges of this new taxation era, neither the system front nor the understanding at all user levels. However, with the passage of time, things are getting stabilised, GST requirements are getting factored in the applicable accounting system of the organization and slowly the new concepts are being digested at all levels. If we analyse this situation, nothing was abnormal and there was only lack of preparedness at both the end, which resulted into the inconveniences tolerated under compulsion across industries. In this article, a small effort has been put-in to place the changes in Works Contract, its practical issues and challenges in during implementation and also post implementation.

Works Contract under Pre-GST:

Works contracts consists of three kinds of taxable activities as per the current law.It involves supply of goods as well as supply of services. If a new product is created during the works contract, then such manufacturer becomes a taxable event.As per the listings, the construction of the building, maintenance, and repairing of plant and machinery, installation, repair, alteration of any movable or immovable property comes under works contract.The details of the taxes under Pre-GST regime are shown below in Fig.1

So, Works Contract, being a single activity are taxed by different laws for its different activities. This causes a lot of confusion regarding treatment and taxability which has resulted many legal disputes in related to works contracts. GST has brought in much needed clarification to this issue in order to put an end to the uncertainty for the legislature.

Implications of Works Contract Under GST:

Section 2 sub Section (119) of CGST defines Works contract means a contract, wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract and includes contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property. GST has removed the confusion regarding the tax treatment. This means works contract will be treated as service and tax would be charged accordingly (not as goods or part goods/part services). This treatment of works contract as service and not as supply of goods has provided much needed clarification to the works contracts.

Points to Remember:

Works Contract concept is attached to Immovable PropertyWorks Contract is a Service, irrespective of Goods & Service proportion and hence SAC (Service Accounting Code) will be applicable.

Now, the linking of concept of Composite Supply with Works Contract and also the concept of Mixed Supply can be understood from the Diagram below in Fig.-2.

Works Contract – GST provision:

Schedule II entry no. 5(b) and 6(a) [Section-7 of CGST Act’2017] talks about what will be treated as “Supply of Service”, wherein Works contract has been specified Clause 5(b) “Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or before its first occupation, whichever is earlier.” Analysis

This clause covers works contract in relation to civil construction. Works contracts in relation to building, complex or any civil structure is treated as supply of service if it is sold before completion of construction.However, if entire consideration on works contract has been received after issuance of completion certificate, where required, by the competent authority or before its first occupation, whichever is earlier than no GST is leviable on such supply as this become immovable property and GST can’t be levied on sale of immovable property

Clause 6 (a) The following composite supplies shall be treated as a supply of services, namely: – (a) works contract as defined in clause (119) of section 2 Analysis This clause has already been explained above under the section “Works Contract under GST”. Here, the most important aspect to be highlighted is that about the impact on the buyer of Real Estate due to GST. In Pre-GST scenario the Service tax on real estate transaction was 4.5% and set off was there for input service tax component and the state composite VAT was varying in different states within the range of (1-4)% on the total property value without any input tax benefit. In Post GST regime, residential construction services, will invite GST at the rate of 12 per cent (with Land value included) and 18% (if Land and Construction Services are separately identified), which will apply to developers selling residential units before completion of construction to the home buyers, where transaction costs increases with higher tax rates, but at the same time input credit is available on both, services and material. Property transaction costs will increase by 6% (with 12% GST), in case no input credit is passed on by developers. If developers pass on the input credit to buyers, the property price increase could be restricted to 1-2%. However, if the developers pass on the credits completely and bring down the base prices, then, home buyers may marginally benefit under the GST regime.

Works Contract – Applicable Tax Rate:

Initially, with the model GST Law, two types of rates were prescribed.

12%-Construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly. [The value of land is included in the amount charged from the service recipient]. In case Land and Construction Services are separately identified, the applicable tax rate on services will be applicable @ 18%.

Other works Contract – 18%

Further, following were the decisions taken by the GST Council in the 22nd meeting held on 6th October 2017 relating to Works Contract.

Works contract services involving predominantly earth works (that is, constituting more than 75% of the value of the works contract) supplied to Central Government, State Governments, Local Authority, Governmental Authority or Government Entity shall be taxed at 5%.The reduced rate of 12% on specified works contract services supplied to the Central Government, State Government, Union Territory, Local Authority and Governmental Authority shall be extended to a Government Entity, where such specified works contract services have been procured by the government entity in relation to the work entrusted to it by the Central Government, State Government, Union Territory or Local Authority.GST shall be levied @ 12% on works contract services in respect of offshore works contract relating to oil and gas exploration and production (E&P) in the offshore area beyond 12 nautical miles.

Works Contract- Input Tax Credit (ITC):

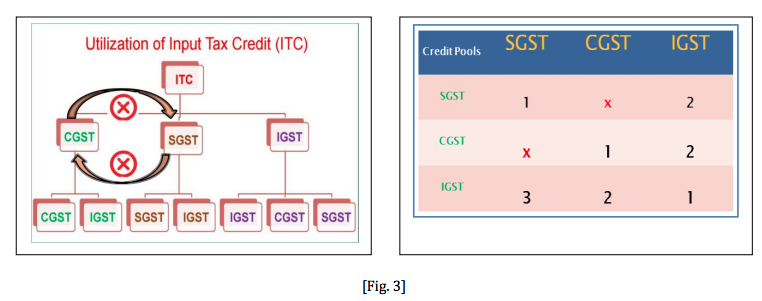

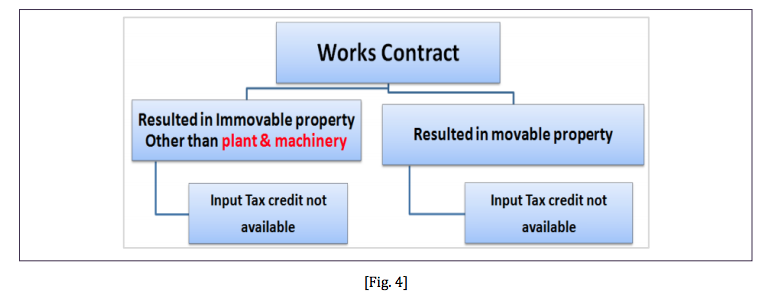

Chapter V of CGST Rules, 2017 talks about Input Tax credit mechanism. One of the biggest advantages expected from the implementation of GST Act is that it would remove cascading effect by facilitating seamless flow of credit. GST Act aims at removing the restrictions placed in the present Cenvat credit rules on availment of credit which lead to break in the credit chain and consequent cascading effect which further leads to increase in cost of goods and services. Under GST, seamless tax credit flow has been ensured by providing for the availment of ITC to the purchasing dealer in respect of the GST paid by the supplying dealer. ITC has been defined as credit of IGST/CGST/SGST charged on any supply of goods and or a service used or intended to be used in the course or furtherance of business and includes the tax payable under reverse charge. Registered taxable person shall be eligible to avail ITC credited to the e-credit ledger subject to condition prescribed without restrictions of availment. The Input Tax Credit (ITC) would be permitted to be utilized in the following manner and as per the marshalling shown in the diagram below in Fig.-3 Section 17 (5) (c) of CGST Act 2017: Input Tax Credit shall not be available in respect of the following, namely: “works contract services when supplied for construction of an immovable property (other than Plant and Machinery) except where it is an input service for further supply of Works contract service” The restriction does not apply to plant and machinery and also in case the input services are further used for supply of Works Contract service under GST (Contractor can avail the ITC in respect of services availed from the sub-contractor). The statement above makes it clear that Input Tax Credit cannot be claimed by the recipient of works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service. The details relating to availability of ITC are summarized through a diagram below in Fig.-4.

Works Contract – Important aspects:

Under model law presently there is no abatement or exemption has been provided in relation to works contract.No RCM mechanism under GST for Works Contract.There is no TDS applicability has been notified so far.Composition Scheme is not applicable for Works Contract.

Works Contract – Practical checklists:

Existing or cut-over contracts as on appointed day need to be amended for factoring in the GST applicability and removing the tax applications of Service Tax, VAT (WCT) etc.The tax code flagging need to be changed in applicable accounting package. The tax code for ITC and Non-ITC works need to be separated for capturing the claims for ITC cases.GSTIN need to be captured in vendor master and its synchronization with the address of the Contractor need to be verified.GSTIN correctness needs to be checked from the GST portal (www.gst.gov.in) under “Search Taxpayer Tab”. GSTIN submitted by the party must appear in portal.The invoice submitted by the Contractor need to be verified for all the mandatory fields prescribed for invoice like- Invoice no.-maximum 16 alphanumeric-special characters, the SAC code, description, GSTIN of both Supplier and Recipient and correct GST claim (CGST & SGST/IGST) along with the tax rate etc.SAC need to be captured in each transaction for getting the relevant details to submit the applicable return with HSN/SAC-wise summary.As the most important aspect for availing ITC is the payment of tax and submission of return by the Contractor to the department, hence the Company also need to ensure the fact that the tax paid to the Contractor has been deposited by him and applicable returns are duly submitted by the Contractor, otherwise the ITC availed by the recipient may need to be reversed. For this, the payment details may be sought from the Contractor and to be checked specifically for the Final Bill.Again, all the Contracts, wherein goods and services are involved and linked to immovable property, need to be brought into the ambit of works contract and to be treated as service, rather than paying tax for goods as per applicable HSN and for services as per applicable SAC Code.Finally, keeping in view the requirements of information for submitting GSTR 3B, GSTR-1 and GSTR-2 along with the Annual Return, the data capturing has to happen at transaction level and necessary reports need to be developed in accounting system. This will help for necessary reconciliation specifically for GSTR 2.

From Contractor perspective:

Conclusion: Change is the only permanent word in this competitive world. However, any change is always difficult to accept, as it takes us away from our comfort zone. But, to move quickly from the tag of developing economy to a developed economy, this Country has to pass through many such changes for creating a transparent, effective and conducive business atmosphere. Perhaps the changes in last few years in terms of New Companies Act, New Indian Accounting Standard (Ind AS) in line with IFRS including the recent GST rollout are right steps forward in this direction. As far as our topic “Practical Implications of Works Contract under GST Law” is concerned, is a mostly discussed area, as there are substantial changes in this area under GST regime. Hence, a structured and conceptual learning on the subject matter is highly essential as Works Contract involves a significant part of the business expenditure, be it capex or opex. Let’s accept the new challenges before us with an attitude to learn, delearn and re-learn, so as to contribute efficiently and effectively to the organisation, we are working for and finally extend our sincerity towards Nation building